AI Agent for Credit Decisioning: Assisted Intelligence for Smarter Lending with Sparkflows

- Apr 21

- 4 min read

What is a Credit Decisioning Agent?

For decades, credit decisioning has relied on manual reviews, static rules, and fragmented tools. While this approach offers control, it often comes at the cost of speed, consistency, and scalability. On the other hand, fully automated systems, while fast, can be difficult to trust in high-stakes financial environments where human judgment still plays a critical role.

This is where a Credit Decisioning Agent built on Sparkflows strikes the right balance.

Rather than replacing humans entirely, the agent functions more like an intelligent application layer, assisting analysts, underwriters, and decision-makers by delivering real-time data-driven recommendations, risk scores, and actionable insights. It automates the heavy lifting of data processing and modeling, while still allowing users to review, validate, and act on the results.

The result is not just automation, but augmented decision-making, where human expertise and AI intelligence work together.

The Problem with Traditional Credit Risk Assessment

Traditional credit evaluation systems are often slow and resource-intensive. Analysts spend significant time gathering data, validating inputs, and applying predefined rules to assess risk.

This manual effort introduces delays and increases operational costs, while also limiting the ability to scale.

At the same time, relying entirely on human judgment can lead to inconsistencies, especially when dealing with large volumes of applications. Subtle patterns in data may go unnoticed, and decision quality can vary across teams.

Fully automated systems attempt to solve these issues, but they introduce another challenge: lack of transparency and control. In regulated industries like finance, institutions cannot afford to rely solely on black-box decisions without human oversight.

What’s needed is a middle ground, a system that accelerates decision-making without removing human accountability.

How the Credit Decisioning Agent Works

The Credit Decisioning Agent in Sparkflows is designed as an assistive workflow, where automation and human input coexist seamlessly.

The system ingests customer data, processes it through a series of transformations, and generates predictive insights. However, instead of directly enforcing decisions, it presents results through an interactive interface where users can review outputs, upload new data, and make final calls.

At a high level, the agent:

Processes applicant data and enriches it with derived features

Calculates credit scores and assigns rating tiers

Predicts risk using machine learning models

Presents results through dashboards and visualizations

Allows users to input new data and validate decisions

This design ensures that the agent acts as a decision support system, not a replacement for human judgment.

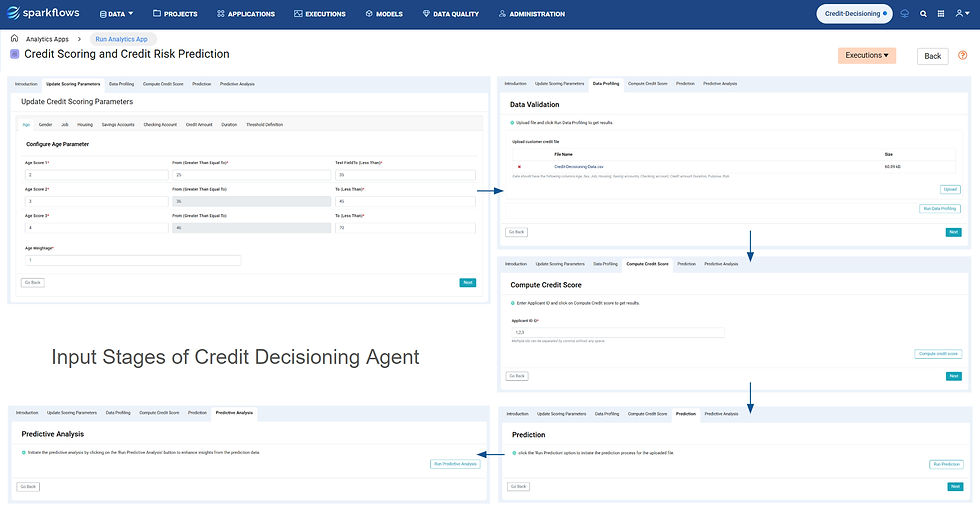

Inputs and Outputs of the Workflow

One of the defining characteristics of this solution is its interactive, app-like nature, where users actively participate in the workflow.

Inputs

The system relies on a combination of structured inputs and user-driven interactions. These include:

Customer demographics such as age, job, and housing status

Financial account details, including savings and checking accounts

Loan-specific information like credit amount, duration, and purpose

Manual uploads of new customer datasets for real-time evaluation

This flexibility allows users to continuously feed new data into the system and analyze different scenarios.

Outputs

Instead of producing rigid, final decisions, the agent generates insight-rich outputs that guide users:

A weighted credit score representing overall creditworthiness

Credit rating categories derived from scoring logic

Risk classification (High Risk / Low Risk) based on model predictions

Visual dashboards showing risk distribution and segment-level insights

These outputs are designed to support, not replace, decision-making by providing users with the context they need to take informed actions.

Inside the Credit Decisioning Pipeline

The workflow is structured as a series of interconnected stages, each contributing to the final outcome while remaining transparent and controllable.

It begins with data preparation, where missing values are handled and relevant features are selected. Feature engineering then transforms raw inputs into meaningful indicators, such as credit scores and rating tiers.

The prepared data is passed into a machine learning model that evaluates risk patterns and predicts the likelihood of default. Finally, the results are presented through interactive dashboards, allowing users to explore and interpret the findings.

Because the system is built in Sparkflows, each stage can be visualized, modified, and extended, making the entire pipeline both flexible and user-friendly.

Modeling and Decision Intelligence

At the core of the agent is a Random Forest model, chosen for its ability to handle complex relationships in financial data. It delivers reliable predictions while maintaining a balance between performance and interpretability.

Instead of relying on rigid rule-based scoring, the model looks at multiple factors together to deliver more balanced and nuanced risk predictions. It captures hidden patterns and relationships that traditional approaches often miss. However, its role is not to replace human judgment but to enhance it.

By combining model predictions with business logic and user oversight, the system ensures that decisions remain both data-driven and accountable.

Business Impact and Insights

As users interact with the Credit Decisioning Agent, it begins to reveal patterns that go beyond individual applications. These insights provide a deeper understanding of the overall credit portfolio.

The analysis shows that a majority of applicants fall into the low-risk category, indicating stability. At the same time, clear distinctions emerge between different borrower segments. Asset-backed loan purposes tend to align with lower risk, while consumer goods financing shows higher default potential.

Financial indicators such as savings account balances play a critical role, with lower balances strongly associated with higher risk. These patterns not only validate the model’s predictions but also provide actionable insights for refining lending strategies.

Because users can continuously upload and analyze new data, the system supports ongoing monitoring and dynamic risk assessment, rather than one-time decisions.

Why Enterprises Are Moving to Assisted Credit Decisioning

Organizations are increasingly recognizing that the future of credit decisioning is neither fully automated nor fully manual, it is assisted.

An agent-based approach allows institutions to:

Accelerate decision-making without losing human control

Improve consistency while retaining flexibility

Reduce manual effort without removing accountability

Adapt quickly to changing business and regulatory requirements

Sparkflows enables this by providing a platform where intelligent workflows can be built as interactive applications, making advanced analytics accessible to business users.

Conclusion

The evolution of credit decisioning is not about replacing humans with machines; it is about enabling better decisions through collaboration between the two.

A Credit Decisioning Agent built on Sparkflows transforms traditional workflows into intelligent, interactive systems that combine automation with human insight. By clearly connecting inputs, predictions, and outcomes, it empowers financial institutions to make faster, smarter, and more transparent lending decisions.

In a world where both speed and trust matter, this assisted approach offers the best of both: efficiency driven by AI and confidence backed by human judgment.

Comments